How Much Should We Trust Staggered Difference-in-Differences Estimates?

Links

Abstract

We explain when and how staggered difference-in-differences regression estimators, commonly applied to assess the impact of policy changes, are biased. These biases are likely to be relevant for a large portion of research settings in finance, accounting, and law that rely on staggered treatment timing, and can result in Type-I and Type-II errors. We summarize three alternative estimators developed in the econometrics and applied literature for addressing these biases, including their differences and tradeoffs. We apply these estimators to re-examine prior published results and show, in many cases, the alternative causal estimates or inferences differ substantially from prior papers.

Important figure

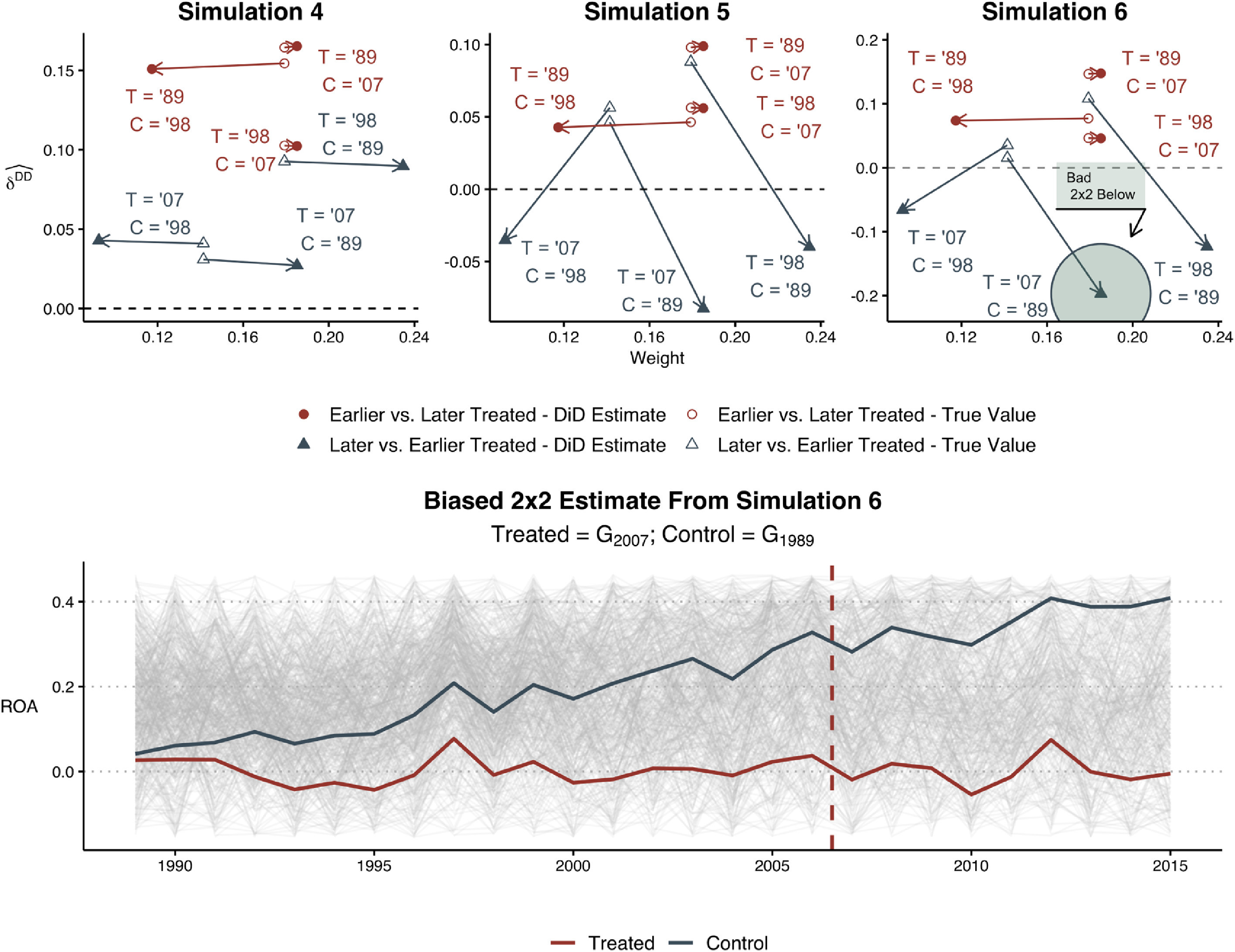

The top panel of Fig. 3 illustrates the diagnostic test for Simulations 4, 5, and 6. Because the diagnostic test only applies to balanced panels, in constructing this figure our simulation is modified to artificially induce a balanced panel of firm-year observations from Compustat before drawing fixed effects and residuals from the empirical distribution.

@article{baker2022much,

title={How much should we trust staggered difference-in-differences estimates?},

author={Baker, Andrew C and Larcker, David F and Wang, Charles CY},

journal={Journal of Financial Economics},

volume={144},

number={2},

pages={370--395},

year={2022},

publisher={Elsevier}

}